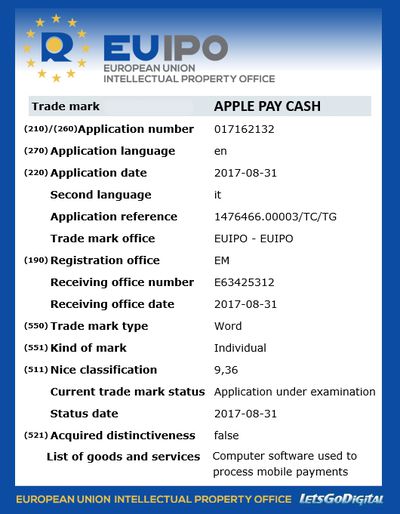

Apple has filed a trademark application in the European Union for Apple Pay Cash, the company's new iMessage-based peer-to-peer payments service coming with iOS 11.

Unearthed by tech blog LetsGoDigital, the application was filed with the European Union Intellectual Property Office (EUIPO) on Thursday and is classified as "computer software for use in connection with electronic payment and funds transfers".

By integrating with iMessage in iOS 11, Apple Pay Cash will enable users to make person to person payments right from within chat threads. To send a cash payment, the user authenticates it with Touch ID (or perhaps via facial authentication on the upcoming "iPhone 8") on their iOS device or Apple Watch.

Money received using the service goes on to an auto-generated virtual Apple Pay cash card, similar to a gift card, that gets stored in the Wallet app. The cash card can then be used to make regular Apple Pay purchases at retail stores and on the web. Alternatively, users will be able to transfer the money to an allocated bank account.

Apple has yet to offer further details on how Apple Pay Cash will work, but Brazilian tech blog iHelp BR has uncovered code references in the Apple Pay framework that suggest users will need to authenticate the service with a driver's license or Photo ID before they can send any money through iMessage. This may be done by holding the ID in front of the camera, similar to when adding a bank card to Apple Pay.

While yesterday's trademark application has yet to be granted by the EUIPO, the fact that it has been filed already may mean Apple Pay Cash will go live across EU countries soon after the initial U.S.-only rollout.

Hopefully we'll know more on September 12, when Apple is expected to launch iOS 11 in tandem with new iPhones, new Apple Watches, and possibly a new 4K Apple TV at its fall event, set to take place at the Steve Jobs Theater in Apple Park.